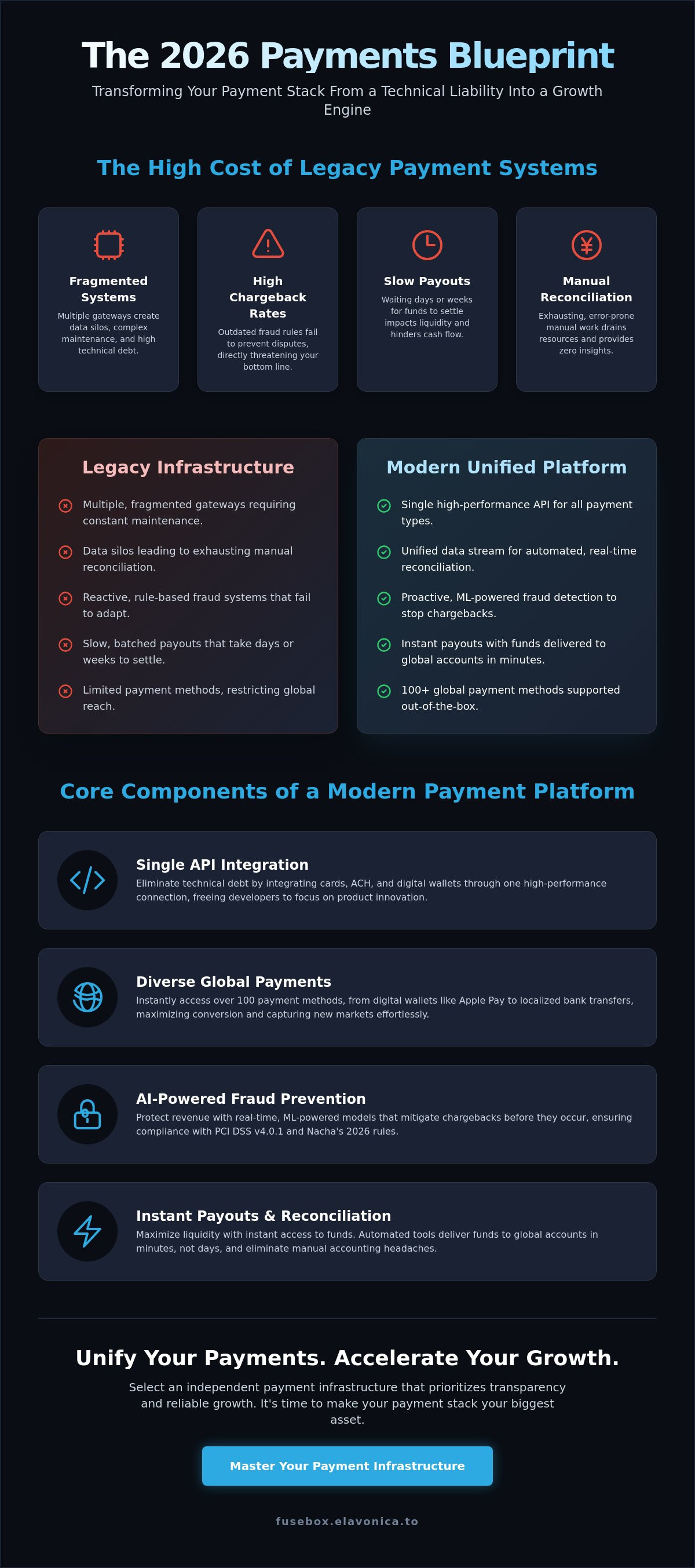

What if your payment stack was a silent engine for growth rather than a source of technical debt? In 2026, online payment processing is the primary differentiator between businesses that scale and those that stall. With PCI DSS v4.0.1 now the mandatory standard and Nacha's new fraud monitoring rules active as of March 2026, the complexity of moving money has never been higher. Fragmented reporting and high chargeback rates are no longer just annoyances; they're direct threats to your bottom line.

You likely feel the pressure of slow payout speeds affecting your cash flow and the exhaustion of manual reconciliation. This guide provides the blueprint to master modern payment infrastructure to secure your revenue and accelerate global growth. We'll explore how to unify your methods via a single API, achieve instant access to funds, and deploy AI-powered fraud detection. It's time to transform your payments into a streamlined, automated asset that values your time as much as your security.

Key Takeaways

- Centralize global transaction management by shifting from legacy gateways to unified commerce platforms.

- Eliminate technical debt by integrating cards, ACH, and digital wallets through a single, high-performance API.

- Protect revenue with real-time, ML-powered fraud detection designed to mitigate chargebacks before they impact your margins.

- Maximize liquidity with instant payouts and automated reconciliation tools that deliver funds to global accounts in minutes.

- Scale securely by selecting an independent online payment processing infrastructure that prioritizes technical transparency and reliable growth.

What is Online Payment Processing in 2026?

Online payment processing is the digital infrastructure that enables businesses to accept, verify, and settle electronic transactions. In 2026, this definition has expanded significantly. It's no longer a simple utility for moving money from point A to point B. It's a strategic layer of unified commerce. Modern infrastructure must handle high-speed verification while maintaining rigorous compliance across global borders. Efficiency in this area directly impacts your net revenue and operational overhead. Every millisecond saved in the authorization loop contributes to higher conversion rates.

The 2026 landscape demands more than basic credit card acceptance. Modern commerce requires native support for diverse payment methods, including digital wallets, localized bank transfers, and emerging real-time payment networks. Businesses now rely on the merchant of record model to navigate the complexities of global trade. This approach offloads the technical and legal burden of local tax compliance and regulatory liability. It allows you to enter new markets instantly. You don't need to worry about the logistics of local entities. Protection and speed are the new industry standards for any scalable business.

The Evolution of Unified Payment Gateways

Legacy systems often relied on fragmented gateways. You might have had one system for web sales and another for mobile or in-person transactions. This created data silos. It led to reconciliation nightmares. Modern online payment processing utilizes a unified gateway architecture. This shift allows for a single API integration that connects your business to over 100 payment methods globally. It simplifies the technical stack. You get a single source of truth for all transaction data. This leads to automated reconciliation and much deeper customer insights. Better data means better business decisions. You can track customer behavior across all channels without manual data merging.

Key Participants in the Payment Lifecycle

The payment lifecycle involves several critical entities working in concert. First is the merchant, who initiates the sale. Next is the Payment Processor, which handles the communication between the merchant and the card networks. The acquirer receives the funds, while the issuing bank authorizes the transaction on behalf of the customer. Understanding this stack is vital for growth. It helps you identify exactly where integration bottlenecks or high fees occur. Independent platforms offer a distinct advantage here. They provide a transparent, no-nonsense layer that ensures transaction integrity. They aren't tied to a single bank's legacy limitations. This independence drives reliability. It ensures your business remains agile and secure as the fintech landscape evolves.

The Core Components of a Modern Payment Processing Platform

A high-performance online payment processing platform is built on technical transparency and modular design. It starts with a single API integration. This is the central nervous system of your commerce engine. Instead of managing dozens of separate connections for cards, bank transfers, and digital wallets, you maintain one. This reduces technical debt. It allows your engineering team to focus on product innovation rather than maintenance. Developer-first tools, including robust SDKs and isolated testing environments, ensure that every update is verified before going live. This precision is what separates modern infrastructure from legacy systems.

Scalability is the second pillar. Your system must handle high-volume spikes without latency. Performance degradation during a flash sale or global launch is unacceptable. Modern platforms utilize cloud-native architecture to auto-scale resources in real-time. This ensures that transaction authorization remains instantaneous regardless of load. When you unify your payment methods, you gain a holistic view of this performance. You can monitor success rates and latency across every channel from a single dashboard. This visibility is essential for maintaining operational speed.

Accepting Diverse Payment Methods

Global growth requires local expertise. Your checkout must support over 100 payment methods to capture diverse markets. Digital wallets like Apple Pay and Google Pay are now essential for mobile conversion. They utilize biometric authentication to bypass traditional form-filling. This reduces cart abandonment significantly. For high-ticket B2B transactions, the resurgence of ACH is driven by its low cost and high reliability. It's the preferred method for large-scale invoices where card fees would be prohibitive. A unified stack allows you to toggle these methods on or off based on regional demand or transaction size.

Infrastructure Reliability and Security

Security isn't just a feature; it's the baseline. Isolated infrastructure and AES encryption are non-negotiable for protecting cardholder data. These technologies ensure that sensitive information is never stored in a vulnerable state. PCI-DSS compliance is a heavy regulatory burden that modern platforms should largely absorb. By using network tokenization, you can process transactions without ever touching raw PAN data. This drastically reduces your audit scope and liability. It protects your business from the reputational damage of data breaches.

Reliability is also defined by how a platform integrates with the broader U.S. Payment Systems. With the acceleration of real-time networks like FedNow, the expectation for immediate settlement has increased. Uptime is the ultimate metric for revenue protection. A platform with 99.99% uptime ensures that your business never misses a sale. This consistent availability builds long-term customer trust and secures your market position. Every component of the stack must function as a silent, powerful engine for your global operations.

Mitigating Risk with Advanced Fraud Prevention

Security is the silent guardian of your revenue stream. In 2026, static, rules-based systems are no longer sufficient to combat sophisticated fraud. Fraudsters use automation to probe for weaknesses; your defense must be equally agile. Advanced online payment processing integrates machine learning (ML) to scrutinize every transaction in milliseconds. This proactive approach identifies threats before they impact your bottom line. It transforms risk management from a defensive hurdle into a strategic advantage.

The true challenge lies in the balance between security and conversion. Overly aggressive filters create false positives. These false declines frustrate legitimate customers and drive them to competitors. Modern infrastructure uses real-time risk scoring to prevent this friction. By analyzing historical data and behavioral patterns, the system makes informed decisions instantly. You protect your revenue without sacrificing the customer experience. High-performance businesses require this level of precision to maintain momentum in global markets.

How ML-Powered Detection Works

ML-powered detection analyzes thousands of data points simultaneously across global networks. It evaluates device fingerprints, IP velocity, and cross-merchant behavioral trends. Every incoming payment request receives a dynamic risk score. High-risk attempts are blocked or flagged for secondary verification. ML fraud detection utilizes adaptive algorithms to distinguish between sophisticated attacks and legitimate consumer behavior, effectively reducing false declines that stifle growth. This continuous learning cycle ensures your defenses evolve alongside emerging threats.

Chargeback Prevention Strategies

Chargebacks are a direct drain on your margins. They result in lost inventory, wasted shipping costs, and escalating merchant fees. 3D Secure 2.0 provides a modern solution for enhanced authentication. It allows for frictionless data exchange between the merchant and the card issuer. This often shifts the liability for fraudulent transactions away from your business. It provides a more secure environment for high-ticket sales. Online payment processing should also include tools for rapid dispute response. Speed is critical when contesting a claim.

Transparency also plays a vital role in risk mitigation. Clear and descriptive billing statements reduce customer confusion. When a shopper recognizes a charge on their bank statement, they're less likely to initiate a dispute. Automated dispute management tools further streamline this process. They aggregate the necessary evidence and submit responses within minutes. This increases your win rate and recovers revenue that would otherwise be lost to "friendly fraud." Efficient risk management is about maximizing your net revenue through intelligent automation.

Optimizing Cash Flow: Payouts and Reconciliation

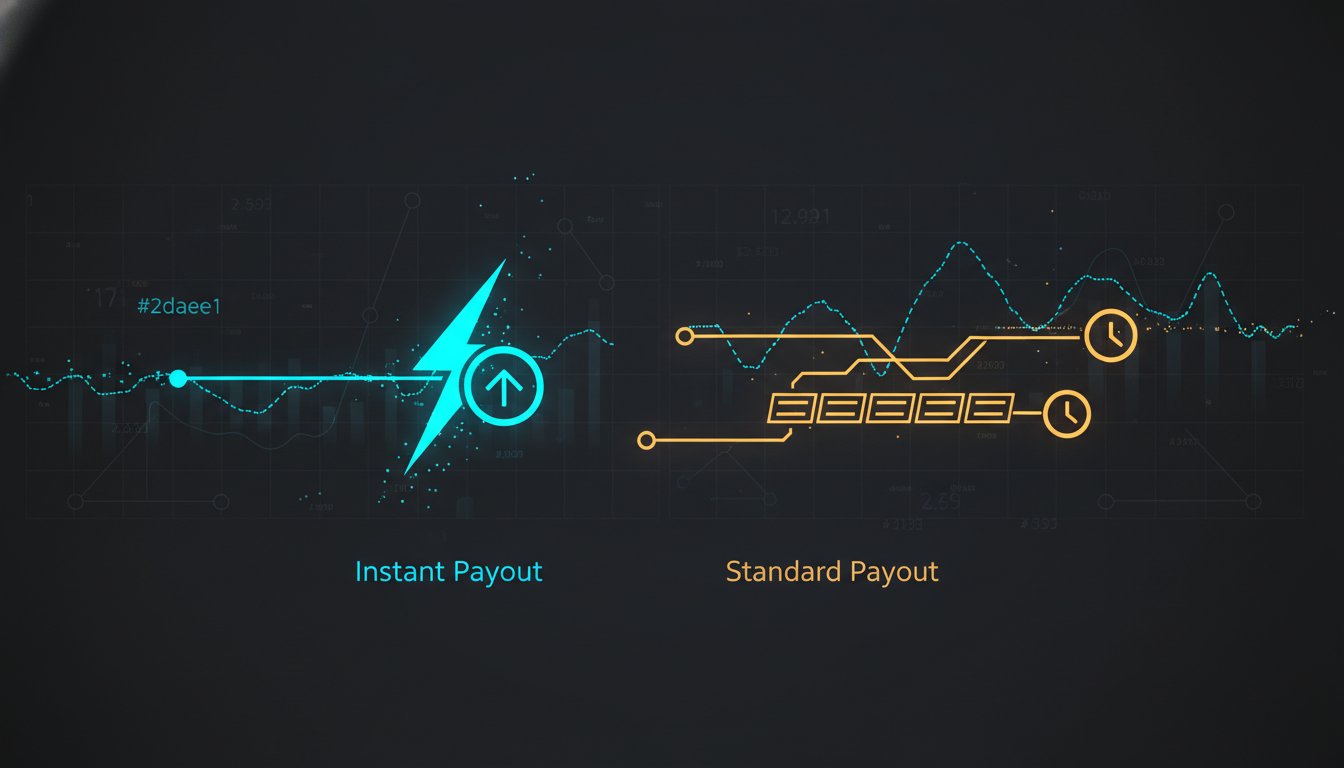

Cash flow is the pulse of your business. Modern online payment processing must do more than just authorize sales. It must accelerate the movement of funds into your bank account. Instant payouts allow you to move capital to bank accounts worldwide in minutes. This speed provides the liquidity needed for immediate reinvestment. You don't have to wait days for legacy settlement cycles. It's about total control over your working capital. Efficiency here is a competitive necessity.

Balancing speed and cost is a strategic decision. Standard transfers remain cost-effective for predictable, long-term operational expenses. However, next-day or instant payouts are now essential for high-velocity environments or urgent vendor payments. Automated reconciliation removes the manual burden of matching payments to invoices. You eliminate the need for error-prone spreadsheets. The system does the heavy lifting. The merchant dashboard provides real-time, data-driven insights that inform your broader financial strategy. It's a single source of truth for your financial growth.

Streamlining Global Payouts

Navigating cross-border payout requirements is notoriously complex. Different countries have varying regulations and tax implications that can stall your momentum. A modern online payment processing stack handles these details automatically. You manage multiple currencies from one dashboard. This transparency extends to fees. You see exactly what it costs to send funds to different destination countries before you hit send. No hidden charges. No surprises. It's a no-nonsense approach to global finance that values your time and your margins.

Unified Invoicing and Payment Tracking

Most providers treat invoicing and payments as separate silos. This creates significant administrative friction and delays in reconciliation. Unified infrastructure allows you to send professional, brand-aligned invoices that natively accept cards and ACH. You track every transaction status in real-time. You see exactly when an invoice moves from "Sent" to "Settled" without checking multiple bank portals or accounting tools. This integration reduces administrative overhead by several hours per week. It ensures your financial reporting is always current and accurate. To start streamlining your financial operations, optimize your payouts and invoicing today.

Selecting the Right Infrastructure for Scalable Growth

Selecting online payment processing is a pivotal business decision. It requires looking past generic marketing claims and surface-level features. Many providers lock you into restrictive ecosystems that limit your agility. Independence matters because it ensures your infrastructure serves your business goals, not the processor's bottom line. Integrity in financial services is built on transparency and technical autonomy. You need a partner that acts as a silent, powerful engine for your global operations. This transition from a utility mindset to a strategic partnership is essential for long-term reliability.

Don't get distracted by the headline base percentage. Effective merchant services pricing includes more than just the transaction rate. You must account for the cost of legacy technical debt, chargeback management fees, and the administrative price of manual reconciliation. A no-nonsense professional evaluation looks at the total cost of ownership across your entire lifecycle. High-volume growth requires a partner that simplifies this complexity rather than hiding it behind dense jargon. Every hidden fee is a friction point in your cash flow that can be eliminated through better infrastructure.

The Elavon Fusebox Approach

Elavon Fusebox provides a unified platform for every transaction type. Whether you're processing online or managing mobile sales, the infrastructure remains consistent and secure. We prioritize professional clarity and operational efficiency above all else. This isn't a friendly guide service. It's a high-performance facilitator for bold innovators. Merchants gain direct access to advanced reporting suites and comprehensive developer tools. This transparency allows your engineering team to build, test, and scale without hitting artificial platform limitations or legacy bottlenecks. You get the tools you need to maintain momentum.

Future-Proofing Your Payments

Consumer preferences and regulatory requirements change rapidly. Your infrastructure must be modular and API-driven to keep pace with global shifts. A rigid system is a liability within an environment defined by real-time payments and digital identity integration. Preparing for the future means choosing a partner that values speed and security as much as you do. Stop treating payments as a utility. Start viewing them as a strategic asset. Moving to a unified, independent platform is the final step in securing your market position. You can sign up for a unified experience at fusebox.elavonica.to to secure your revenue and accelerate global growth.

Secure Your Financial Infrastructure for 2026

Modern commerce demands more than just moving money. It requires a resilient, unified architecture that absorbs technical complexity. By consolidating your stack through a single API and deploying ML-powered fraud detection, you protect your margins and your reputation. Speed remains the ultimate differentiator. Instant payouts ensure your capital is always available for reinvestment, effectively removing the friction of legacy settlement cycles. These efficiencies allow you to focus on product innovation rather than payment logistics.

Mastering online payment processing is no longer optional for businesses targeting global scale. It's the silent engine of your operational efficiency. Elavon Fusebox provides the independent, high-performance infrastructure required to navigate this complex landscape. You gain access to over 100 payment methods, real-time risk management, and automated reconciliation tools designed for modern merchants. Streamline your payments with Elavon Fusebox and transform your financial stack into a strategic asset. Secure your revenue and accelerate your global business growth today.

Frequently Asked Questions

What is the difference between a payment gateway and a payment processor?

A payment gateway is the front-end technology that captures, encrypts, and routes transaction data. The payment processor is the back-end engine that facilitates communication between the merchant, the card networks, and the banks to settle funds. Modern platforms often combine these functions into a single, unified layer to reduce technical friction and improve data accuracy.

How long does it take to integrate a modern payment API?

Integration speed depends on your technical requirements and the complexity of your existing stack. Developer-first APIs allow for basic connectivity in a few hours. Full production deployment, including rigorous testing and compliance verification, typically occurs within a few business days. Modular documentation and comprehensive SDKs are essential for accelerating this timeline and ensuring a secure connection.

Can I accept ACH and credit card payments through the same platform?

Unified platforms allow you to accept credit cards, digital wallets, and ACH transfers through a single API connection. This centralization eliminates the need for fragmented reporting across multiple providers. It ensures that all transaction data flows into one dashboard for automated reconciliation. You gain a holistic view of your revenue without managing separate systems for different payment methods.

What are the typical fees associated with online payment processing?

Total costs for online payment processing consist of non-negotiable interchange rates, network assessment fees, and the processor's markup. Interchange fees are set by card networks like Visa and Mastercard. Assessment fees are paid directly to those networks. The markup is the negotiable portion that covers the technical infrastructure, security features, and payouts provided by your partner.

How does ML-powered fraud detection reduce chargebacks?

ML-powered detection analyzes thousands of transaction patterns and behavioral data points in real-time to assign a risk score to every request. By identifying anomalous behavior across global networks, the system blocks fraudulent attempts before they're authorized. This proactive approach reduces chargeback rates and protects your business from the escalating fees associated with high dispute ratios.

What is an instant payout and how does it work for merchants?

Instant payouts move settled funds to your bank account in minutes rather than the standard two to three business days. This process utilizes real-time payment networks to bypass legacy settlement cycles. It provides immediate liquidity for operational expenses and reinvestment. You gain total control over your working capital by accessing your revenue as soon as a transaction is verified.

Is PCI-DSS compliance included with my payment processing service?

Leading processors provide the secure infrastructure and tokenization required to help you maintain PCI-DSS v4.0.1 compliance. While you're ultimately responsible for your own compliance status, using a secure platform reduces your regulatory burden. It ensures that sensitive cardholder data never touches your servers. This drastically narrows your audit scope and protects your business from liability.

Can I use one dashboard to manage both online and in-person payments?

Unified commerce platforms allow you to manage both online and in-person transactions from a single administrative dashboard. This centralization provides a holistic view of your sales performance and customer behavior across all channels. It simplifies reporting and reconciliation by ensuring that all data is synchronized in real-time. You eliminate the administrative overhead of manual data merging from separate sources.