In 2026, your payment stack is no longer a back-office utility. It's the primary engine of your platform's growth. Most leaders realize that fragmented payment methods and rising developer overhead are actively stalling global expansion. Maintaining multiple integrations while defending against 2026's sophisticated fraud threats is an operational drain. You need a modern payment infrastructure for platforms that prioritizes speed and security over manual maintenance.

We understand the pressure to move money faster while staying compliant with the latest PCI DSS v4.0.1 standards and Nacha fraud rules. This guide provides the blueprint to master the architectural components required to scale your operations. You'll learn how to turn a technical necessity into a high-margin revenue stream. We'll examine the shift from fragmented to unified stacks and provide a roadmap for single-API integration. You'll also discover exactly how to monetize payments as a platform to maximize your bottom line.

Key Takeaways

- Define the critical gap between basic gateways and high-performance, platform-grade infrastructure to support complex money movement.

- Simplify global scaling by consolidating over 100 payment methods through a single, developer-friendly API integration.

- Evaluate the strategic shift toward a unified payment infrastructure for platforms that balances modular control with rapid scalability.

- Future-proof operations with instant payout capabilities and multi-rail routing strategies designed for the 2026 regulatory landscape.

- Discover how an independent engine like Fusebox Portal provides the modularity needed to manage complex fund flows securely and efficiently.

What is Payment Infrastructure for Platforms?

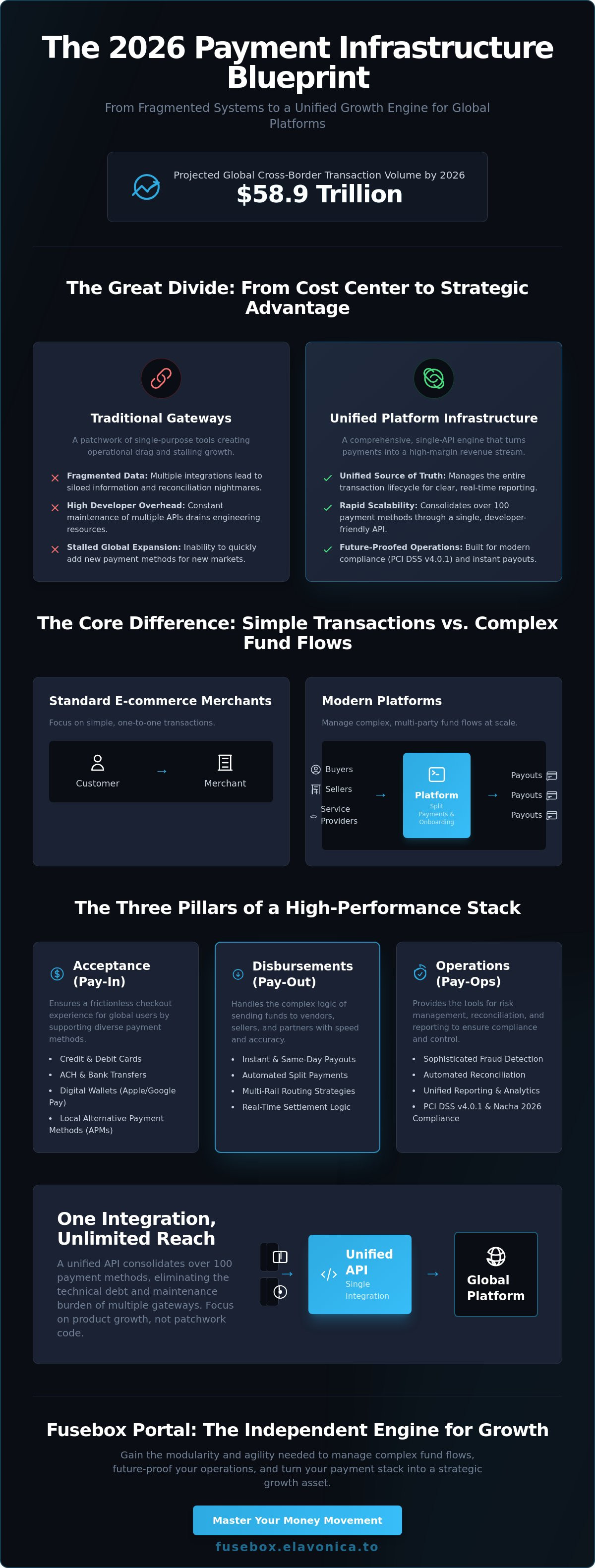

Modern payment infrastructure for platforms is the invisible engine driving global commerce. It is far more than a basic payment system used to accept credit cards. Instead, it represents a comprehensive network of APIs, financial rails, and compliance layers that facilitate complex money movement. In 2026, global cross-border transaction volumes are projected to reach $58.9 trillion. This massive scale requires a technical foundation that prioritizes speed, security, and modularity. Your infrastructure dictates your ability to move funds across borders without operational friction.

Many leaders confuse a standard payment gateway with platform-grade infrastructure. A gateway is a single-purpose tool. It simply moves data from a checkout page to a processor. In contrast, platform infrastructure manages the entire lifecycle of a transaction. It handles multi-party fund flows, automated payouts, and sophisticated risk management. Without a specialized payment infrastructure for platforms, businesses face fragmented data and high developer overhead. High-performance infrastructure turns payments from a cost center into a strategic advantage.

The Core Difference: Merchants vs. Platforms

Standard e-commerce merchants focus on one-to-one transactions. A customer pays, and the merchant receives the funds. Platforms operate on a much higher level of complexity. They manage multi-party flows involving buyers, sellers, and service providers. This requires sophisticated split-payment logic to distribute funds accurately across multiple stakeholders in real time. It's about managing the flow, not just the transaction.

Effective infrastructure must handle sub-merchant onboarding at scale. It requires the ability to verify identities and manage risk across thousands of individual accounts simultaneously. Unified reporting is also critical. Platform leaders need a single, clear view of all financial activity to maintain operational control. This transparency ensures that reconciliation doesn't become a bottleneck as the user base grows. It's about building for the next million users, not just the next thousand.

Key Components of a Robust Stack

A high-performance payment stack consists of three primary pillars. Each serves a specific functional purpose in the money movement lifecycle. These components must work in perfect synchronization to ensure stability.

- Acceptance (Pay-In): This layer supports diverse payment methods including cards, ACH, and digital wallets. It ensures a frictionless checkout experience for global users. In 2026, this must include support for local alternative payment methods to capture global market share.

- Disbursements (Pay-Out): This component handles the logic of sending funds to vendors or partners. It must support immediate settlements to meet modern industry standards. Delayed payouts are no longer acceptable in a real-time economy.

- Operations (Pay-Ops): This includes tools for fraud detection, reconciliation, and reporting. Modern Pay-Ops must comply with PCI DSS v4.0.1 and Nacha 2026 rules. This ensures every transaction is correctly categorized and monitored for sophisticated threats.

By integrating these components into a unified payment infrastructure for platforms, you eliminate the need for multiple, disjointed integrations. You gain the agility to launch new revenue models and expand into new territories with minimal technical debt. It's the difference between struggling with legacy systems and leading the market with a modern, independent engine.

The Architecture of Modern Money Movement

Architecture determines whether a platform scales or breaks. Modern payment infrastructure for platforms must handle high-velocity fund flows across global rails. It requires a foundation that abstracts technical complexity. Centralizing these operations reduces data fragmentation and operational silos. This clarity allows your team to focus on product growth rather than legacy code maintenance. With global cross-border transaction volumes expected to reach $58.9 trillion by 2026, your architecture must be ready for massive scale.

Success in 2026 demands a shift from patchwork systems. You need a single source of truth for every transaction, whether it happens online or in-person. A unified approach ensures financial data stays synchronized in real time across all channels. Immediate reconciliation is only possible when your infrastructure handles automated data normalization. It creates a seamless path for money to move from customers to your platform and out to your partners without manual intervention.

Unified API: One Integration, Unlimited Reach

Technical debt stalls expansion. Integrating multiple gateways for different regions or payment types creates a heavy maintenance burden. A unified API solves this by consolidating over 100 payment methods into one entry point. You can launch in new markets in days. Access global credit cards, ACH, and local alternative methods through a standardized interface. This modularity is essential for staying competitive in a fast-moving market.

Standardized data formats simplify your backend engineering. Developers use one set of protocols for all global operations. This efficiency leads to faster deployment and lower costs. A single point of contact provides the flexibility to add features without rebuilding your core logic. To optimize your technical roadmap, see how the independent architecture of Fusebox Portal consolidates your global footprint through a developer-friendly API.

ML-Powered Fraud & Risk Management

Rule-based fraud detection is obsolete. Static logic cannot keep pace with 2026's automated threats and sophisticated cybercrime. You need a risk layer that learns. Machine learning models analyze millions of data points across your ecosystem to identify patterns before they hit your bottom line. This proactive approach is essential for protecting margins. It ensures compliance with the latest Nacha 2026 fraud monitoring rules while maintaining high transaction speeds.

The goal is balancing security with conversion. Aggressive filters frustrate users and kill revenue. ML systems refine their accuracy to reduce false positives significantly. By identifying the subtle differences between high-risk transactions and high-value customers, you protect the platform without compromising the experience. This level of precision is a mandatory requirement for modern payment infrastructure for platforms. It allows you to scale safely while providing a frictionless experience for legitimate users.

Embedded vs. Unified Infrastructure Models

Choosing between embedded and unified models is a decision between convenience and control. Many platforms start with embedded payments to simplify the user experience. This model integrates a third-party brand's full financial stack directly into your interface. It's a fast way to launch, but it often leads to ecosystem lock-in. You sacrifice long-term flexibility for short-term ease. A unified payment infrastructure for platforms offers a modular alternative. It uses a central engine to manage diverse rails while keeping your platform at the center of the strategy.

A unified model provides the transparency that embedded systems often obscure. It allows you to route transactions through multiple providers without changing your core integration. This independence is critical for platforms that plan to scale globally. It ensures you aren't tied to the pricing or technical limitations of a single acquirer. By maintaining a modular stack, you retain the power to optimize margins as your volume grows. It's about building a foundation that supports your roadmap, not the vendor's.

Evaluating the "Build vs. Buy" Dilemma

Building a proprietary stack from scratch carries massive hidden costs. You don't just build code; you build a compliance department. As of June 2026, all 64 requirements of PCI DSS v4.0.1 are mandatory. Maintaining these standards requires continuous security monitoring and expensive annual audits. The "Build" route often results in significant technical debt and diverted engineering resources. It's a high-risk path for platforms that need to move fast.

Leveraging existing infrastructure provides an immediate time-to-market advantage. You outsource the regulatory burden and security overhead to experts. This allows your team to focus on core product features that drive user value. A hybrid approach is often the most efficient. By using white-label infrastructure, you maintain full brand control while benefiting from a battle-tested engine. You get the reliability of a mature system with the flexibility of a custom-built solution.

The Strategic Advantage of Independence

Independence from major acquirers provides significant leverage in fee negotiations. If you're locked into a single ecosystem, you have no recourse when rates increase. An independent payment infrastructure for platforms allows you to switch or add processors without a total rebuild. This flexibility is a powerful tool for protecting your margins. It ensures your platform remains agile in a shifting financial landscape.

Transparency in reporting is another major benefit of an independent stack. You get unbiased data across all your payment channels. This clarity simplifies reconciliation and provides a single source of truth for your financial operations. A partner that acts as a "silent engine" empowers your brand rather than competing with it. You provide the experience, while the infrastructure handles the complexity of global money movement behind the scenes.

- Avoid vendor lock-in to maintain negotiation leverage.

- Outsource compliance to reduce operational risk and cost.

- Keep your brand front and center with white-label modularity.

Future-Proofing Your Platform: 2026 Requirements

By 2026, standard payment processing is no longer sufficient. Platforms must adapt to a landscape defined by real-time expectations and complex regulatory oversight. A future-proof payment infrastructure for platforms must be agile enough to integrate emerging rails and automated compliance tools without disrupting the core user experience. Speed is the new baseline. Security is the non-negotiable floor. Your ability to adapt to these shifts dictates your market share.

Success requires a move toward total automation. Manual intervention in fund flows creates bottlenecks that scale poorly. Modern architecture must handle the heavy lifting of routing, compliance, and reconciliation automatically. This allows your engineering team to focus on innovation rather than maintenance. It's the only way to stay competitive in a market where transaction volumes and complexity continue to accelerate.

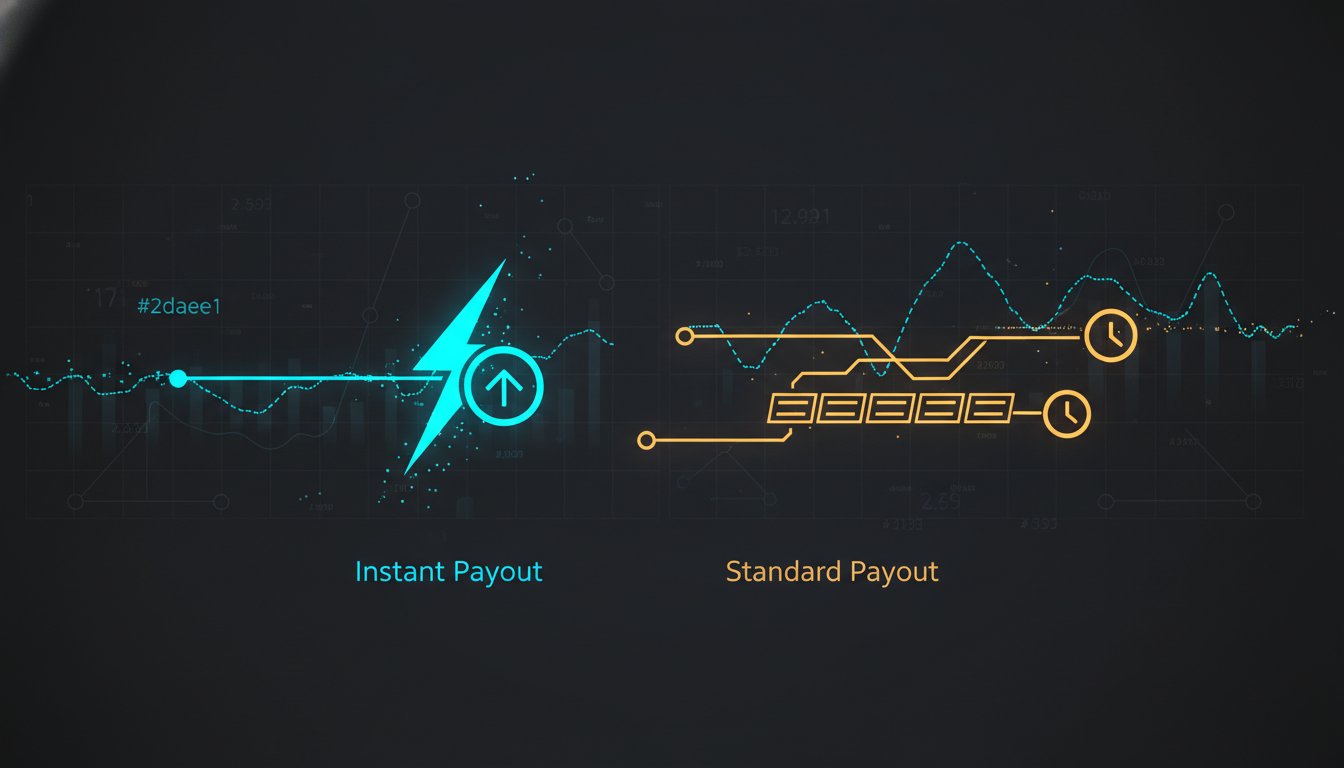

The Demand for Instant Payouts

Platform users in 2026 don't wait for "next-day" settlements. They expect funds to be available the moment a transaction clears. Instant bank transfers have become a primary driver for partner retention and platform loyalty. If your payouts are slow, your partners will migrate to competitors who offer immediate liquidity. It's a direct correlation between payout speed and platform growth. Speed has become a product feature in itself.

Accelerated payout speeds require sophisticated liquidity management. High-performance infrastructure provides the visibility needed to manage these risks effectively. You gain the ability to offer faster access to funds while maintaining strict operational control. This balance is critical for long-term stability. It ensures you can meet user demands without compromising your own financial health. Automated payout logic reduces the risk of human error during high-volume periods.

Dynamic Routing and Multi-Rail Capability

Multi-rail payments are the ability to switch between networks like ACH and FedNow automatically based on transaction priority and cost. Selecting the optimal payment rail is no longer a manual process. Dynamic routing engines analyze cost, speed, and reliability for every transaction in real time. This ensures every dollar moves through the most efficient channel available. It's a strategic approach to cost management that protects your margins.

The rise of real-time rails like FedNow has fundamentally changed platform architecture. It enables immediate settlement for high-priority transfers while utilizing traditional ACH for lower-cost flows. This flexibility ensures you aren't overpaying for speed when it isn't required. A multi-rail strategy also provides the redundancy needed to ensure uptime during network outages. It's about building operational resilience into your core stack. Modernize your payout strategy with Fusebox Portal to access immediate settlement and multi-rail routing today.

Navigating cross-border regulations requires automated tools that update in real time. Manual compliance is a liability in 2026. Integrating automated invoicing into your core payment flow further reduces friction. It ensures that billing and reconciliation happen simultaneously. This eliminates the need for separate accounting software integrations and simplifies your backend operations. You achieve a leaner, more efficient financial operation that is ready for the next decade of growth.

Fusebox Portal: The Independent Engine for Growth

Fusebox Portal delivers the modularity required for a high-performance payment infrastructure for platforms. It acts as a silent, powerful engine that eliminates the friction of managing multiple integrations. You gain access to over 100 payment methods through a single interface. This independence ensures you remain in control of your financial strategy. It provides the technical foundation to move money globally while maintaining complete operational integrity.

The platform is built for extreme scale. It handles complex fund flows with precision, ensuring every transaction is routed efficiently. Advanced fraud detection layers protect your margins automatically by identifying threats in real time. Global payout tools ensure your partners receive funds immediately, meeting the 2026 standard for liquidity. You receive professional support from experts who understand the unique challenges of platform-grade commerce. It is the definitive solution for businesses that value speed and reliability.

Seamless Integration for Developers

Speed to market is a competitive necessity. Our REST API design prioritizes technical clarity and rapid deployment. It abstracts the complexity of global financial rails into a single entry point. Developers can implement a robust payment infrastructure for platforms without the burden of months of custom coding. This efficiency reduces technical debt and allows for faster product iterations. Integration is straightforward, secure, and built for modern engineering workflows.

Manage your entire ecosystem from a comprehensive dashboard. It provides real-time reporting and automated reconciliation for every account. This visibility is essential for high-volume online payment processing operations. You see every transaction, payout, and risk event in one centralized location. It serves as the single source of truth for your financial operations. Data is standardized, making backend engineering simpler and more reliable.

Scaling Your Platform with Confidence

Fusebox Portal supports your growth from the first transaction to global market leadership. Our infrastructure handles increasing complexity without performance degradation. You gain a transparent partner focused on operational reliability and technical excellence. There is no unnecessary fluff; just a secure, technologically advanced foundation for your business. This stability allows you to focus on user acquisition while we manage the complexity of money movement.

Future-proof your platform today with an engine designed for the 2026 economy. Review our API documentation to see the technical specifications and integration protocols. Contact our sales team for a custom walkthrough of our platform-grade capabilities. Build your business on infrastructure that prioritizes your independence and long-term success. Secure your margins and accelerate your growth with Fusebox Portal.

Modernize Your Financial Architecture

The transition from fragmented gateways to a unified payment infrastructure for platforms is no longer optional. Leaders must prioritize modularity to eliminate technical debt and capture global market share. You've seen how independent engines prevent vendor lock-in and provide the transparency needed for real-time reconciliation. By 2026, the ability to manage complex money movement through a single entry point will separate market leaders from legacy survivors. Your architecture is the primary engine of your operational scale.

Fusebox Portal provides the technical foundation to execute this strategy with precision. Access a unified API supporting over 100 payment methods. Protect your margins with integrated ML-powered fraud detection and execute global payouts to bank accounts worldwide. It's time to turn your payment stack into a high-margin revenue engine that fuels long-term growth. Explore Fusebox Portal Infrastructure and start scaling your operations with confidence. Your platform's growth depends on the strength of its foundation.

Frequently Asked Questions

What is the difference between a payment gateway and payment infrastructure?

A payment gateway is a single-purpose tool designed to move transaction data from a checkout page to a processor. In contrast, payment infrastructure for platforms is a comprehensive system that manages multi-party fund flows, automated payouts, and compliance layers. Infrastructure handles the entire financial lifecycle, whereas a gateway only addresses the initial pay-in step for a single merchant.

How does payment infrastructure support platform monetization?

Infrastructure supports monetization by automating the collection of transaction fees and managing complex split-payment logic. It allows platforms to take a percentage of every transaction while distributing funds to sub-merchants in real time. This technical foundation enables the launch of tiered service models and embedded financial products that drive recurring revenue without manual intervention.

Why is a single API integration important for scaling platforms?

A single API integration eliminates technical debt by consolidating over 100 payment methods into one entry point. This reduces developer overhead and speeds up time-to-market for new regions. Platforms can scale globally without rebuilding their core stack every time they add a local payment method or currency, ensuring that engineering resources remain focused on product innovation.

What are the main types of payment rails used in platform infrastructure?

Platform infrastructure typically utilizes card networks like Visa and Mastercard, traditional ACH, and emerging real-time rails like FedNow. High-performance stacks use dynamic routing to select the optimal rail based on cost and speed for every transaction. This ensures that high-priority payouts move through immediate rails while standard transactions utilize lower-cost networks to protect margins.

Can payment infrastructure help reduce chargebacks and fraud?

Robust payment infrastructure for platforms reduces risk by analyzing data patterns across your entire user base. It identifies suspicious behavior before transactions settle, which significantly lowers chargeback rates. Automated fraud monitoring ensures compliance with Nacha 2026 rules, protecting the platform and its partners from sophisticated threats through real-time risk assessment and mitigation.

What should I look for in a global payout solution for my platform?

Prioritize solutions that offer immediate settlement and support for multiple currencies across global bank accounts. A global payout engine must handle the complexity of local regulations and tax reporting automatically. Reliability is paramount; ensure the provider offers a transparent, independent engine that avoids vendor lock-in and provides clear, unified reporting for all financial activity.

Is it better to build or buy payment infrastructure for a new SaaS platform?

Buying infrastructure is the strategic choice for most SaaS platforms due to the extreme cost of regulatory compliance. Maintaining PCI DSS v4.0.1 standards requires continuous security monitoring and expensive annual audits. Leveraging an existing engine allows your engineering team to focus on core product features rather than the heavy lifting of backend financial maintenance and security.

How does ML-powered fraud detection differ from traditional methods?

Traditional fraud detection relies on static, rule-based logic that often fails against modern, automated threats. ML-powered systems use machine learning to identify evolving patterns across millions of data points. This approach increases accuracy, reduces false positives, and ensures that legitimate users experience zero friction. It provides a proactive defense that learns from every transaction in the ecosystem.